Reviews by year

According to the results of the stress tests, euro area banks have sufficient capital adequacy even in the event of the realisation of adverse macroeconomic shocks. These stress tests are performed every other year under the auspices of the European Central Bank (ECB) and the European Banking Authority (EBA) and included the two significant Slovenian banks. The stability and capital adequacy of the Slovenian banking system are also indicated by the stress tests carried out by Banka Slovenije for other Slovenian banks and savings banks, which followed a similar methodology.

More informations in press release.

Banka Slovenije and the ECB are continuing their efforts to include climate risks in the performance of their key tasks. So it was that the ECB conducted climate risk stress tests for the largest European banks this year, and an exercise for the other banks. The exercise was also conducted at Banka Slovenije for the smaller banks and savings banks along the lines of the ECB model. These are the first stress tests and exercises of their kind, and are primarily aimed at raising awareness and understanding and identifying weaknesses. At the ECB level and in Slovenia too they primarily revealed the need for better quality of and access to data, and for the inclusion of climate risks in the internal processes of the commercial banks.

More informations in press release.

Euro area banks have sufficient capital adequacy, according to the stress tests conducted at significant banks under the aegis of the ECB. The stress tests, in which the two largest Slovenian banks were also included, show banks retaining high resilience even under the adverse scenario. Comparable tests were conducted for smaller banks and savings banks at Banka Slovenije, and showed similar results.

This year’s stress tests thus confirm the stability of the Slovenian banking system, which is disclosing sufficient capital adequacy.

More informations in press release.

The EU-wide stress tests planned for this year under the aegis of the EBA, the ECB SSM and Banka Slovenije have been postponed until next year because of coronavirus. Banka Slovenije is well aware of the importance of monitoring key risks at the level of individual banks and savings banks, and at the level of the banking system, and has therefore decided to conduct liquidity stress tests (LiST). Liquidity risk has been highlighted on several occasions as one of the three key risks (alongside credit risk and capital risk) that will affect banks the most over the short and medium terms.

The methodology is based on the ECB’s targeted liquidity stress tests from 2019, with a top-down approach. The scenarios used (an adverse scenario and an extreme scenario) are based on previous liquidity crises, and were calibrated for all European countries by the ECB. Banka Slovenije has made the scenarios even harsher. The banks’ results are evaluated through a survival period, and a normalised net liquidity position at the end of the test horizon. Given the need to regularly monitor liquidity risk in extreme situations, we will repeat these calculations every quarter.

The analysis completed in July and September reveals that the banks’ liquidity position remains sound under the baseline scenario. The survival period at the most exposed banks is shortening under the adverse scenario. Here it should be noted in particular that the survival period remains relatively long and ensures that there is sufficient manoeuvring room to potentially make adjustments to liquidity positions and to carry out mitigation measures.

Evropski bančni organ (EBA) vsaki dve leti, nazadnje v letu 2018, izvaja vseevropske stresne teste bank. V vmesnem letu 2019 se je Evropska centralna banka (ECB) v okviru Enotnega mehanizma nadzora (SSM) in v skladu z že uveljavljeno prakso odločila, da izvede ciljne stresne teste, ki so bili letos osredotočeni na likvidnostno tveganje. V vajo so bile vključene tudi vse pomembne slovenske banke (SI) pod neposrednim nadzorom ECB. Za manj pomembne slovenske banke (LSI) in hčerinske banke v večinski tuji lasti je po vzoru ECB stresne teste izvedla Banka Slovenije.

Primarna mera likvidnostnega tveganja v okviru stresnih testov je obdobje preživetja ("survival period"), merjena v dneh, ko neto likvidnostna pozicija postane negativna. Obdobje preživetja je časovno obdobje, znotraj katerega institucija lahko uporabi svoja likvidna sredstva na način, da preživi nenaden likvidnostni šok. Praviloma naj bi se institucija znotraj tega časovnega obdobja aktivno prilagajala na načine (ukrepi, procesi), ki bi zagotavljali njeno dolgoročno poslovanje. Banka Slovenije je za posamezne banke na osnovi denarnih tokov in scenarijev izračunala, ali bodo v šestmesečnem obdobju likvidnostni odlivi presegli prilive, upoštevajoč tudi sekundarno likvidnost. Poleg obdobja preživetja je bila izračunana tudi neto likvidnostna pozicija ("funding deficit/surpluss"), merjena kot odstotek celotnih sredstev.

Na ravni sistema so banke izkazovale dobro likvidnostno pozicijo, predvsem zaradi visoke ravni sekundarne likvidnosti. Z izvedbo stresnih testov je Banka Slovenije dobila bolj podroben vpogled v likvidnostno pozicijo posamezne banke, rezultati stresnih testov pa bodo po vzoru SSM vključeni tudi v skupno oceno tveganosti institucije.

Stresni testi v letu 2019 so bili po obsegu in kompleksnosti precej manj zahtevni kot stresni testi leto poprej, kljub temu pa se je tudi letos pokazalo, da morata razumevanje podatkovnih zahtev in skrb za večjo kakovost podatkov ostati ena od prioritet bank in nadzornikov.

V letu 2018 je Evropski bančni organ (EBA), v sodelovanju z Evropskim odborom za sistemska tveganja (ESRB), Evropsko centralno banko (ECB) ter Enotnim nadzornim mehanizmom (SSM), po enoletnem premoru zopet izvedel vajo vseevropskih stresnih testov bank.

Cilj vseevropskih stresnih testov je zagotoviti nadzornikom, bankam in drugim udeležencem na trgu skupen analitičen okvir za ustrezno primerjavo in oceno odpornosti evropskih bank in evropskega bančnega sistema na neugodne razmere na trgu. Rezultati letošnjih stresnih testov vključujejo tudi učinke prehoda bank na uporabo novega računovodskega standarda MSRP 9 s 1. 1. 2018. Prag uspešnosti izvedbe letošnjih stresnih testov, merjen s količnikom kapitalske ustreznosti, ni bil določen. Se pa rezultati stresnih testov upoštevajo kot eden od vhodnih elementov v okviru procesa rednega pregledovanja in ovrednotenja tveganj banke, ki ga vsako leto izvedejo pristojni nadzorniki.

V vajo je bilo vključenih 48 največjih sistemsko pomembnih bank (70 % EU bančnega sistema), od katerih jih 33 sodi pod neposredni nadzor SSM. Slovenske banke zaradi majhnosti (prag za vključitev je bil najmanj 30 mrd EUR bilančne vsote) v vajo stresnih testov EBE niso bile vključene. Vaja stresnih testov EBE se je pričela konec januarja 2018, banke pa so rezultate stresnih testov v več zaporednih ponovitvah posredovale v obdobju od konca maja do oktobra 2018. Po izvedenem procesu preverjanja kakovosti rezultatov so bili rezultati stresnih testov, vključno z individualnimi rezultati bank, objavljeni na spletni strani EBE dne 2. 11. 2018.

Več o scenarijih, metodologiji, obrazcih in vzorcu vključenih bank si lahko ogledate na spletni strani:

https://www.eba.europa.eu/-/eba-launches-2018-eu-wide-stress-test-exercise

Pristojni nadzornik vsako leto izvede proces rednega nadzorniškega pregledovanja in ovrednotenja tveganj (SREP proces), katerega pomemben element so tudi stresni testi. Posledično bo SSM:

- za pomembne banke, ki sodelujejo v stresnih testih EBE, v SREP proces vključila rezultate stresnih testov EBE,

- za pomembne banke, ki niso vključene v stresne teste, izvedla lastne stresne teste.

Slovenske pomembne banke (NLB, NKBM in Abanka) so vključene v stresne teste pod okriljem SSM. Z namenom zagotovitve enake obravnave vseh pomembnih bank v okviru SSM (v vzorcu in izven vzorca stresnih testov EBE), so tudi banke vključene v SSM stresne teste v popolnosti sledile metodologiji EBE. Rezultati SSM stresnih testov ne bodo javno objavljeni.

V Banki Slovenije smo v skladu z utečeno prakso iz prejšnjih let izvedli stresne teste za preostale banke, ki so v neposredni pristojnosti Banke Slovenije (manj pomembne banke, hranilnice, SID banka in banke hčere v večinski tuji lasti). Banka Slovenije je pri izvedbi stresnih testov upoštevala velikost in kompleksnost slovenskih bank ter ustrezno poenostavila Ebino metodologijo in obrazce. V skladu s prakso SSM tudi rezultati stresnih testov slovenskih manj pomembnih bank ne bodo javno objavljeni.

Stresni testi v letu 2018 so pokazali, da se kakovost izvedbe stresnih testov s strani slovenskih bank počasi izboljšuje, da pa še vedno obstajajo področja, ki bi jih bilo mogoče v prihodnje nadgraditi. Banka Slovenije bo posledično banke še naprej spodbujala k boljšemu razumevanju procesa, metodologije in poročevalskih zahtev stresnih testov, zagotovitvi ustreznih kadrovskih in tehnoloških resursov ter razvoju lastnih modelov in napovedi.

The EBA did not conduct EU-wide stress tests of banks in 2017, in line with its approach and timetable. Within the framework of the SSM, a decision was therefore made to focus on interest rate risk in the banking book (IRRBB) in 2017 for the purposes of SREP stress tests. The Bank of Slovenia also embarked on stress tests in 2017 on the ECB model. All less significant banks (LSIs) and subsidiary banks under majority foreign ownership were included in the Bank of Slovenia stress tests.

Interest rate risk

Interest rate risk in the banking book is based on the calculation of the impact of a change in the interest rate curve on the economic value of equity (EVE) and on net interest income (NII) at an individual bank. The changes and developments in interest rates assumed in the stress tests are theoretical, and do not represent a forecast of interest rate developments in the future. The stress tests are designed to assess the sensitivity of an individual bank to such changes. The methodology for calculating sensitivity takes account of the attributes of the individual bank’s interest-sensitive products (contractual attributes and attributes deriving from client behaviour models). EVE and NII are the basic metrics for calculating interest rate risk in the banking book.

The stress tests conducted by the Bank of Slovenia for 2017 for the aforementioned banks were primarily based on banks’ regular supervisory reports and on an approach that to the greatest possible extent reflected the ECB SSM methodology for IRRBB stress tests in 2017. The approach provided for partial horizontal comparability between Slovenia’s three systemically important banks (NLB, NKBM and Abanka), and the other less significant institutions. The Bank of Slovenia’s approach allowed for the inclusion of individual calculations and attributes of Slovenia’s LSIs on the basis of a special questionnaire aimed at examining the implementation of IRRBB at individual institutions.

Findings

The results of the Bank of Slovenia’s IRRBB stress tests were largely similar to the ECB’s stress test results for the entire SSM. Interest rate risk is present, but is manageable at the system level. Banks and savings banks had relatively closed interest-sensitive positions on the cut-off date, which they additionally closed by allocating the stable portion of sight deposits.

The results of the stress tests reveal a positive impact (i.e. an increase) in the banks’ interest income in the event of a rise in interest rates over the next three years.

For more about the ECB approach, see the ECB sensitivity analysis of IRRBB – stress test 2017.

In accordance with Article 100 of the CRD IV, which requires supervisors to conduct annual stress tests, the Bank of Slovenia again conducted bottom-up stress tests of the banking system in 2016. The stress tests are part of regular supervisory activities.

The stress tests in 2016 were aimed at identifying key risks at the individual tested banks and savings banks. The findings of the stress tests were used as one of the input parameters in the annual supervisory review and evaluation process (SREP) at the individual bank or savings bank. Risks are assessed at the bank or savings bank on the basis of the SREP, and appropriate measures are taken where necessary.

Banks covered

All banks and savings banks classed as LSIs, including SID banka and the subsidiary banks under majority foreign ownership, were included in the stress tests conducted between 18 March and 20 July 2016. NLB and NKBM were included in the parallel stress tests conducted under the aegis of the ECB, which also followed the EBA methodology, while stress tests were conducted on Abanka within the framework of the comprehensive assessment of the bank owing to its classification as an SI in 2016.

Findings

In general, the 2016 stress tests revealed a lack of qualified staff, knowledge and experience to be a common problem for Slovenian banks (including the significant banks). The banks were also weak in the areas of model support and adequate databases.

For more, see: Section 3.6.5 of the Bank of Slovenia’s 2016 Annual Report (Stress tests).

In accordance with established practice, the Bank of Slovenia again conducted stress tests of the entire banking system in 2015.

Banks covered

All banks and savings banks were included in the stress tests, with the exception of UniCredit Banka Slovenija, which conducted stress tests as part of the comprehensive assessment of the bank under the supervision of the ECB. The banks drew up their calculations on the basis of the proposed methodology and assumptions, and submitted them to the Bank of Slovenia. The quality and consistency of the data, the application of the methodology and the technical accuracy of the calculation were vetted for the calculations received.

The general assumptions and methodology drawn up by the EBA for the EU-wide stress tests in 2014 were taken into account in the stress tests. The scenarios were implemented on the basis of consolidated data from the closing accounts for 2014. The time horizon was three years (2015, 2016 and 2017).

Requirements

The definitions of the highest-quality form of capital (common equity Tier 1) and capital requirements applicable inside the stress test horizon were used in the calculation of capital ratios and capital. In their calculations the banks did not take account of activities to mitigate the effects of shocks, other than the recapitalisations carried out by 31 May 2015. The minimum capital adequacy requirement as measured by the highest-quality form of capital (the common equity Tier 1 capital ratio) was 8% under the baseline scenario and 5.5% under the adverse scenario.

Findings

On the basis of the assumptions under the baseline scenario, all the banks remained solvent and maintained a common equity Tier 1 capital ratio above the threshold value. Under the adverse scenario four banks disclosed a small capital shortfall owing to the failure to meet the threshold capital ratio. All the banks with a shortfall took action in 2015 to improve their capital position.

For more, see: Section 3.6.7 of the Bank of Slovenia’s 2015 Annual Report (Stress tests)V Banki Slovenije smo v skladu z utečeno prakso tudi v letu 2015 izvedli stresne teste celotnega bančnega sistema.

EU-wide stress tests were conducted in 2014 before the introduction of the SSM, the new single supervisory mechanism for significant European banks under the aegis of the ECB, which came into being on 4 November 2014.

Aim of the comprehensive assessment

Before taking over the supervision of significant banks the ECB wanted to obtain a clear picture in particular of the quality of the investments and the adequacy of capital coverage in the event of a deterioration in business conditions at each significant bank or banking group. To ensure that standard procedures were applied in the comprehensive assessment at all significant banks in the euro area, a detailed standard methodology for asset review and valuation was drawn up and stress tests were centrally formulated for each country with regard to the various macroeconomic circumstances. The huge project of conducting a simultaneous comprehensive assessment of all 130 selected significant banks began in early 2014, under central management at the level of the ECB and in close collaboration with the national banking supervisors. The entire project consisted of three parts: an asset quality review, stress tests, and the determination of capital requirements in light of the results of the two preceding phases of the assessment. The results of the comprehensive assessment were simultaneously published for all the banks at the end of October, just before the SSM entered into force on 4 November 2014.

Banks covered

The three largest Slovenian banks (NLB, NKBM and SID banka) were included in the assessment.

Results

The findings of the comprehensive assessment of the banking system, including the asset quality review and the stress tests conducted on the cleaned-up assets, were expressed as a capital shortfall or surplus. None of the Slovenian banks would have disclosed a capital shortfall at the end of 2016 under the baseline scenario of the stress test. The total capital surplus of the three banks under the baseline scenario amounted to EUR 754.7 million. Two banks (NLB and NKBM) would have disclosed a small capital shortfall of EUR 65 million at the end of 2016 under the adverse scenario, while SID banka would again have disclosed a capital surplus under the adverse scenario. Measures were adopted at the two banks with a small capital shortfall, and the effects of forbearance improved profitability in 2014 to the extent that the identified capital shortfalls would be covered by retained earnings.

The findings of the comprehensive assessment of the banks’ operations confirm that the clean-up of bank balance sheets and recapitalisation in 2013 were executed to the minimum sufficient extent to ensure resilience in the event of the realisation of adverse economic developments, and to an optimal extent from the point of view of public spending. The balance sheet clean-up and recapitalisation were already yielding results: the two banks were profitable and performing well in 2014, which was also improving their capital positions.

Methodology:

Results:

- ECB: Results of the 2014 comprehensive assessment

- ECB Press release, 26 Oct 2014: ECB’s in-depth review shows banks need to take further action

- Banke Slovenije Press release, 26 Oct 2014: Two Slovenian banks with minor capital shortfalls in 2016 under the stress tests have their shortfalls covered by means of restructuring and retained earnings

- EBA: EU-wide stress testing 2014

In light of the adverse situation in the economy, speculation about the recapitalisations required by Slovenian banks, and the European Commission’s recommendations, a comprehensive assessment of the banking system was conducted in 2013. On 10 April 2013 the European Commission published the results of the in-depth review for Slovenia (Macroeconomic Imbalances Slovenia 2013) with the finding that excessive macroeconomic imbalances exist in Slovenia, and called for an asset quality review and stress tests.

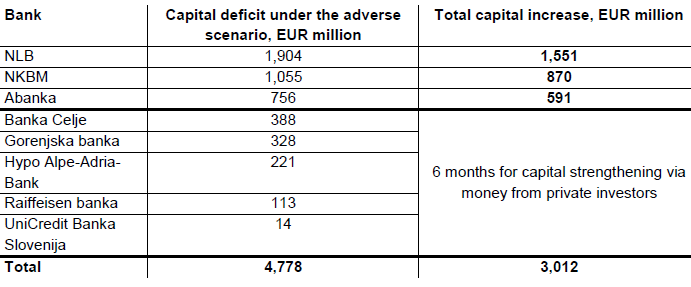

Banks covered

Alongside the three systemically important banks (NLB, NKBM and Abanka), the exercise as a whole also covered seven other banks on the basis of the predetermined criteria. Those banks were: Gorenjska banka, Banka Celje, UniCredit Banka Slovenija, Hypo Alpe Adria Bank, Raiffeisen bank, Probanka and Factor banka. The last two were only involved to a limited extent, in line with their orderly wind-down processes.

Providers

The Bank of Slovenia hired Oliver Wyman to conduct the bottom-up stress tests, Deloitte and Ernst & Young for the AQR, Roland Berger to conduct top-down stress tests, and several independent appraisers for real estate valuations. By hiring specialist independent external institutions, the Bank of Slovenia ensured an independent review and objective assessment of the capital shortfall in accordance with the requirements of the European Commission and the Council.

A decision was taken whereby the Bank of Slovenia would cover the costs of stress tests for all ten banks included in the exercise, and the costs of an AQR for banks that did not request aid in accordance with the Government Measures to Strengthen Bank Stability Act (the ZUKSB). The three banks that requested aid under the ZUKSB bore the costs of the AQR themselves.

Methodology

The subject of the AQR was the verification of data completeness and integrity, a review of individual loans, collateral valuation and the identification of impairment shortfalls. The results of the AQR also served as the basis for the bottom-up stress tests. The aim of the stress tests was to assess the capital shortfall/surplus of individual banks under the baseline and adverse scenarios for a three-year projection period (2013 to 2015).

Results (identified capital shortfall under the adverse scenario)

Based on the AQR, negative equity was identified at all five banks (NLB, NKBM, Abanka, Factor banka and Probanka) as a result of the additional impairments that they were required to create. Failure to recapitalise the banks (to cover the aforementioned negative equity and to ensure that the banks meet the minimum required capital adequacy) would have been followed by the initiation of bankruptcy proceedings against the banks, and the associated requirement to repay deposits covered by guarantee.

Measures

In accordance with the ZBan-1 and taking into account the conditions for state-funded recapitalisation, the Bank of Slovenia adopted decisions on 18 December 2013 imposing the following emergency measures on five banks:

- the extinction of qualified liabilities (equity and subordinated liabilities of the aforementioned banks); and

- the recapitalisation of the banks in question in the form of state aid to cover outstanding losses and ensure capital adequacy.

Summary of decisions (full text in Slovene):

Reports and documentation:

Stress tests results:

- Bank of Slovenia and Slovenian government announce results of stress tests, 12 December 2013

- Press conference video 12 December 2013

- Statement by the President of the Eurogroup on Slovenia, 12 December 2013

- Statement by Vice President Rehn on the publication of results of stress tests of Slovenian banks, 12 December 2013

Capital increases:

- Government carries out capital increases at five banks following European Commission approval, 18 December 2013

- Full report on the comprehensive review of the banking system (short version)

- Frequently asked questions and answers regarding the reorganisation of the Slovenian banking system

- Cost of the comprehensive review of the banking system (Feb., 2014)

Methodology:

Full report:

EU-wide transparency exercise 2013

With the aim at restoring confidence, fostering market and supervisory discipline and promoting financial stability European Banking Authority (EBA) in autumn 2013 conducted the EU-wide transparency exercise. 64 banks that were already part of the recapitalisation exercise in 2012 participated in the exercise, including Nova Ljubljanska banka d.d., Ljubljana and Nova Kreditna banka Maribor d.d. The information includes data on banks' composition of capital, composition of RWAs, exposures to sovereigns, credit risk, market risk and securitisation as well as and Loan To Value (LTV) across portfolios as at 31December 2012 and 30 June 2013.

Results:

More: 2013 EU-wide transparency exercise

Bank of Slovenia Stress Tests 2013

EU Capital Exercise 2011/2012

On 26 October 2011 the European Council agreed on measures to restore stability and confidence in the banking sector. Within this framework, policy measures prepared by the European Banking Authority (EBA) with regard to banks exposure to the Member Countries of the European Economic Community (ECC) were adopted to strengthen the capital positions of European banks.

The adopted measures require that banks strengthen their capital positions by building up a temporary capital buffer against sovereign debt exposures to reflect current market prices, without taking into account prudential filters on sovereign assets in the Available-for-Sale portfolio. In addition, banks will be required to establish a buffer so that Core Tier 1 capital ratio reaches a level of 9% by the end of June 2012. The amount of the sovereign capital buffer identified and reflection of market prices used therewith is based on 30 September 2011 figures.

Nova Ljubljanska banka d.d. and Nova Kreditna banka Maribor d.d. are the two Slovenian banks participating in the sample of 71 European Union banks.

Results of EU wide recapitalisation exercise:

- Update on the implementation of the capital exercise (Press Release, 11 July 2012)

- More EBA: Update on the implementation of Capital Plans following the EBA’s 2011 Recommendation on the creation of temporary capital buffers to restore market confidence (11 July 2012)

Final report on the implementation of the recapitalisation exercise 2011

The EBA Recommendation on the creation of temporary capital buffers to restore market confidence was adopted by the Board of Supervisors on 8 December 2011 to address the difficult situation in the EU banking system, especially with regard to the sovereign exposures, by restoring stability and confidence in the markets. The Recommendation was part of a suite of measures agreed at EU level.

The Recommendation called on National Authorities to require banks included in the sample to strengthen their capital positions by building up an exceptional and temporary buffer such that their Core Tier 1 capital ratio reaches a level of 9% by the end of June 2012. In addition, banks were required to an exceptional and temporary capital buffer against sovereign debt exposures to reflect market prices as at the end of September 2011. The amount of the sovereign capital buffer has not been revised.

The results of both banks including in the exercise regarding the final assessment of the capital exercise and fulfilment of the EBA December 2011 Recommendation show the following:

- Final report on the implementation of the recapitalisation exercise (Press Release: 3 October 2012)

See also EBA: EU Capital exercise final results

EU wide stress testing exercise 2011

The European Banking Authority (Eba) in cooperation with the national supervisors (in Slovenija Banka Slovenije), the European Central Bank (ECB), the European Commission (EC) and the European Systemic Risk Board (ESRB) conducted the EU-wide stress test with the aim to restore confidence in the sound EU banking sector. In Slovenia this year, two largest banks, namely Nova Ljubljanska banka d.d. and Nova Kreditna banka Maribor d.d. have participated in the EU-wide stress test.

- Results: NLB, NKBM

- Disclosure of the outcome of the EU-wide stress test for the Slovenian banks (Press Release: 15. July 2011)

EU wide stress testing exercise 2010

Based on the mandate given by the EU Economic and Financial Affairs Council (ECOFIN), the exercise, coordinated by the Committee of European Banking Supervisors (CEBS), was conducted in ninety one European banks in cooperation with the national supervisory authorities and the ECB. The exercise was targeted at covering at least 50% of the individual banking system. On this basis, six banks from the Republic of Slovenia were tested.

Additional information on the outcome of the stress test conducted in Nova Ljubljanska banka can be found in the Press release (23 Jul 2010) and in the following documents:

- Disclosure of the outcome of the EU-wide stress test for the Slovenian bank (Press Release,23 July 2010)